Rough Market: Letseng's Production Falls, While Prices Remain Stable

Post Date: 26 Jul 2010 Viewed: 469

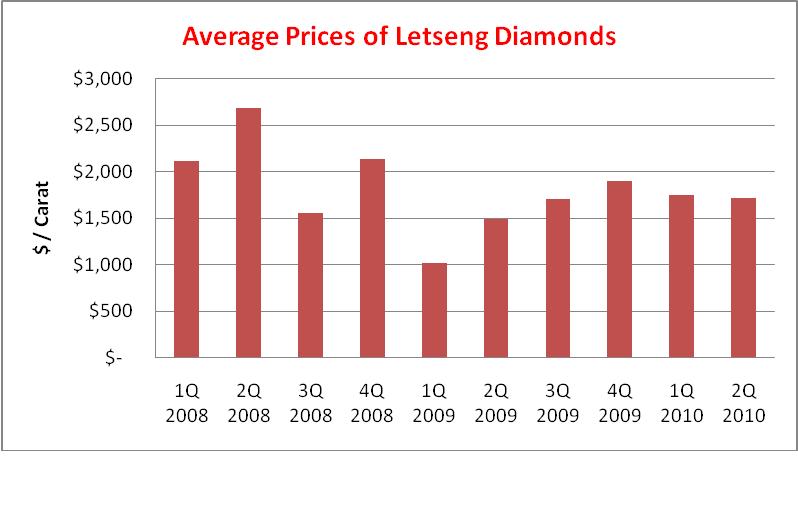

Prices for rough from Gem Diamonds’ Letseng mine, considered to yield the diamonds with the highest per-carat value in the world, remained essentially stable in the second quarter of 2010, compared to the first, at $1,714 per carat. Prices were 14 percent higher than those achieved in the second quarter of 2009, but 36 percent below those recorded for the same period in 2008. Letseng, located in Lesotho, is 70 percent owned by Gem Diamonds, with the local government holding 30 percent.

Production at the mine fell 5 percent year over year to 44,748 carats during the second quarter. Gem Diamonds’ chief executive officer (CEO) Clifford Elphick explained that fluctuations in output were expected due to the mine’s high value and low diamond content.

With the aim of increasing revenue, the mine plan was revised during the half year to allow a higher proportion of ore to be sourced from the satellite pit, but kimberlite instabilities resulted in limited access to the pit. Gem Diamonds added that higher-than-average rainfall and an illegal strike also contributed to the decline in production.

Despite the lower output, the company said it is confident that its target levels will be achieved for the year through the continued strong recovery of smaller diamonds and scheduled access to higher-grade satellite pipe material toward the end of the year.

Still, Letseng continued to produce high-priced goods, with the top ten selling stones from the mine ranging in price from $31,562 per carat to $58,724 per carat. A total of 245 rough diamonds larger than 10.8 carats were sold from Letseng during the half year.

Manufacturing & Wholesale: India’s Uptrends

India’s polished and rough diamond trade continued to gain in the second quarter of 2010 and has comfortably exceeded even 2008 levels. The data collected from monthly reports published by the Gem & Jewellery Export Promotion Council (GJEPC) confirms reports of a strong recovery in India’s diamond manufacturing and trading sectors.

Polished exports rose 85 percent year on year to $5.94 billion in the three months that ended on June 30, 2010 and were 57 percent above the value posted for the second quarter of 2008. The increase was driven by the higher prices achieved on India’s polished as the average price of the exports, $420.73 per carat, represented a 70 percent increase against the same quarter of 2009 and a 13 percent rise compared with 2008. The trend reflects the country’s movement toward dealing in more expensive goods, rather than a general trend in polished prices. Volumes grew at a more subdued pace.

Similar trends were seen in India’s polished imports, which rose 88 percent to $3.69 billion, twice the value achieved in 2008. The average price for the imports, $356 per carat, was 28 percent above the 2009 level and 44 percent higher than that of the second quarter of 2008.

Rough imports grew 63 percent to $3 billion, around the same level as in 2008. The average price of the rough rose 11 percent year on year to $68.37 per carat, but remained 4.5 percent below the 2008 average.

Retail: Bidz.com Continues Declines

Bidz.com, an online jewelry retailer, reported that it expects revenue to total $25 million in the second quarter that ended on June 30, 2010, compared with revenues of $26.9 million for the same period of last year. The 7 percent decline marks a continued downtrend for the company, as sales have dropped through each of the previous five quarters.

Bidz further forecasted to report a loss of 2 cents to 3 cents per share during the second quarter compared to a profit of 3 cents a share in 2009.

Given its market space, the company should be in a stronger position as online buying has been a growth point for the industry and less affected by the downturn than the brick and mortar jewelry sector.

It is therefore unclear what has influenced the move into the red and more details should be revealed when the full results are released on August 9.

Global Markets

United States: Wholesale activity has been quiet, but trading is expected to improve, beginning at the New York Jewelry Association show (JA) next week. Even if expectations for the event are restrained, many are hoping it will signal the start of a busier second half. Buying by retailers has been very selective so far. Retail demand remains focused on bridal goods.

Belgium: With the August break approaching, the market is quiet, as expected. Traders have already shifted to vacation mode, after a week shortened by the public holiday. Some sellers have been more flexible on prices in a bid to close some last-minute deals. There is stable demand for 0.30- to 3.99-carat goods, while 4.00-carat goods remain weak.

Israel: Trading continues to be slow as the August vacation period approaches. Some are taking the opportunity to attend to tasks they would not have time for during busier periods, such as office renovations. There is some level of business being conducted, but caution is evident, with manufacturers expressing concern about rough shortages and low profit margins. There is good demand for oversize stones in the 1.25-carat-plus sizes and stable demand for 0.30- to 0.70-carat, 1.00-carat, 3.00-carat and 5.00 carat goods in F+, VS+. Demand from the U.S. is focused on melee- to 1.50-carat goods, SI1-I1.

India: The polished market has slowed as buyers appear to be expecting prices to soften. Demand is focused on the smaller goods, with melee, J+, SI-pique goods being strong items. There is overall good demand for 1.00-carat goods, although demand and prices for 1.00-carat, VS+ goods has softened slightly. In the rough market, there is stable activity in clivage goods. Manufacturing profits are being squeezed as rough prices remain high, however, with reports of further increases this month.

China: The market continues to be quiet as is expected through July and early August. The mood among wholesalers and retailers is subdued, but traders are confident business will pick up again later in August. Demand is relatively stable and focused on 0.30-carat to 1.10-carat, D-J, VVS-SI, Gemological Institute of America (GIA)-certified and preferably EX stones. There is sporadic demand for 1.00-carat and 1.50-carat, D, IF stones with GIA certificates and for diamonds over 3.00 carats.

Hong Kong: Traders appear to be taking time to assess the market as manufacturing centers have slowed their activity during the summer months. Business is driven by specific item buying and there is very little stock purchasing at the moment. Activity is expected to increase toward the end of August as buyers start to prepare for the September Hong Kong show.

Quote of the Week

“The problem is not that there are problems. The problem is expecting otherwise and thinking that having problems is a problem.”